ABI November 2020: Business conditions at architecture firms backslide from October

However, firms remain modestly optimistic about 2021

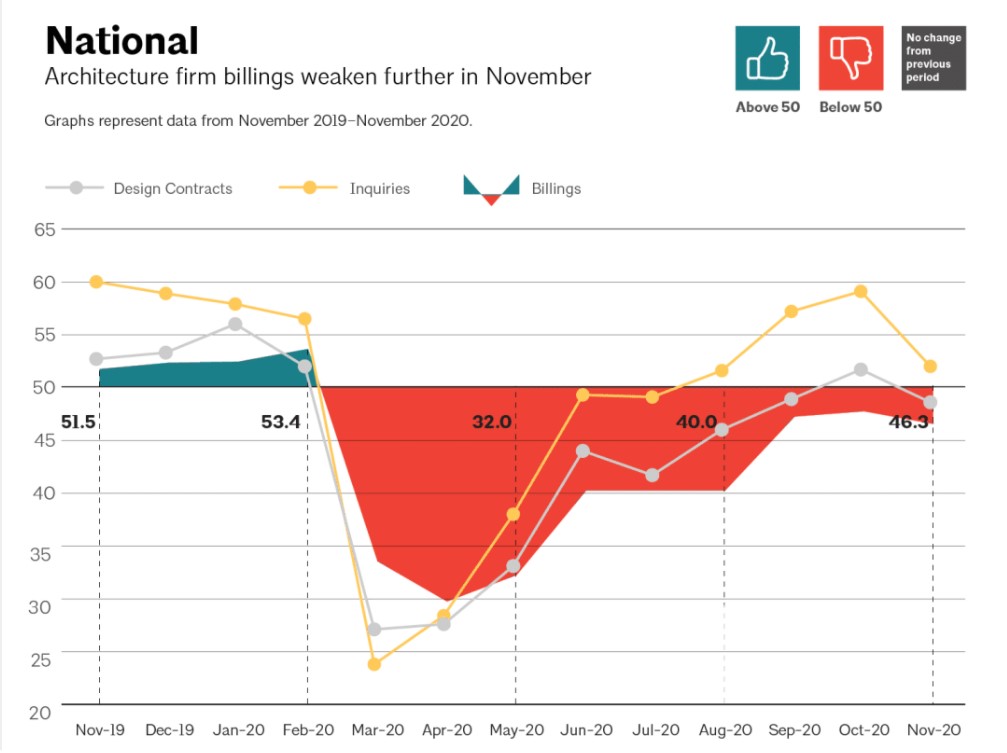

Architecture firm billings declined for the ninth consecutive month in November. The ABI score of 46.3 for the month indicates that the pace of the billings decline accelerated from October, after moderating in September and October (any score below 50 represents a decline in firm billings). The recent increase in COVID-19 cases over the last several weeks seems to have put a damper on the nascent recovery, and also appears to be reflected in a decline in the value of new design contracts in November, following their first increase since February last month. In addition, while inquiries into new work continued to rise, the pace of that growth slowed substantially from the previous two months. Together, these signs indicate that client interest in new projects has started to wane after more encouraging signs last month.

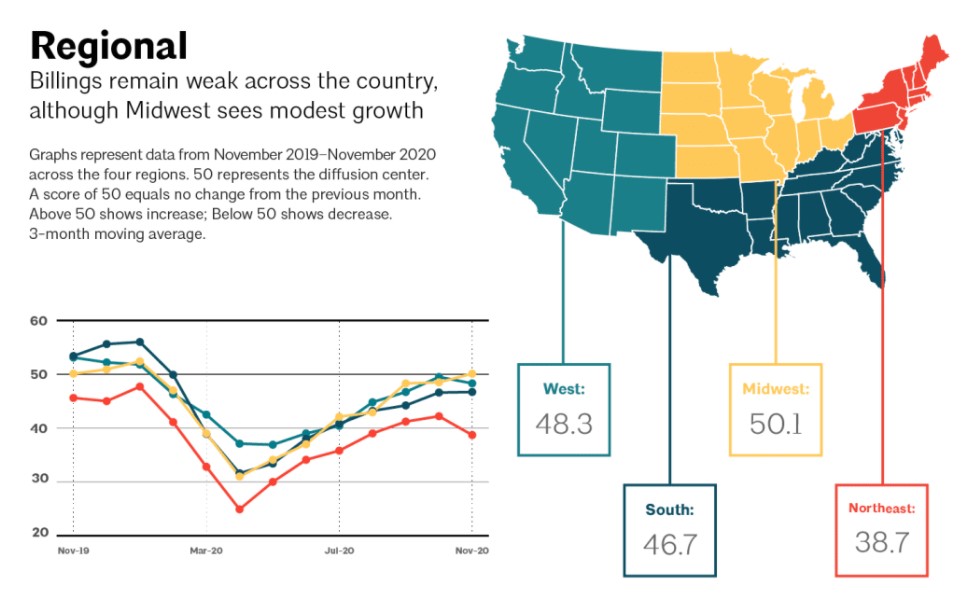

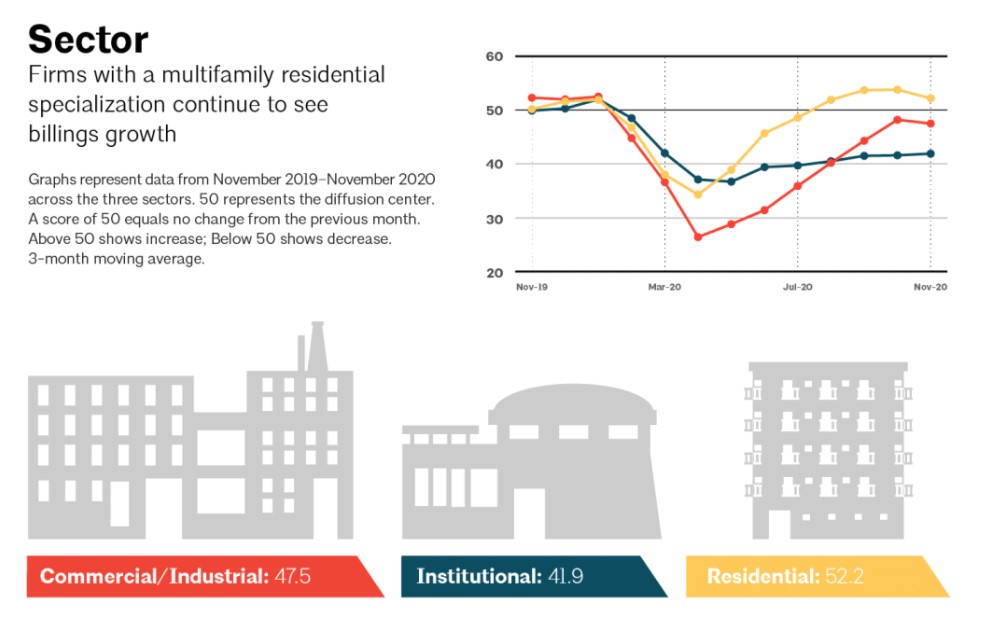

Business conditions also remained soft across much of the country in November, with billings weakening most noticeably at firms located in the Northeast, which were also hardest hit earlier in the pandemic. However, architecture firms in the Midwest saw their billings rise slightly for the first time since January. In addition, this month firms with a multifamily residential specialization saw modest growth for the fourth consecutive month, as that sector remains the one bright spot amid the pandemic-induced downturn. But billings continued to decline at both firms with commercial/industrial and institutional specializations, with firms with a commercial/industrial specialization seeing a less dramatic decline, likely due to increased demand for distribution, logistics, data centers, and other industrial facilities recently.

Growth in a few key sectors

In the broader US economy, nonfarm payroll growth slowed substantially in November, with just 245,000 new jobs added, versus 610,000 in October. Despite strong gains throughout much of the summer and early fall, nonfarm payroll employment remains nearly 10 million jobs below its February pre-pandemic peak. Construction employment increased by 27,000 in November, and is now 279,000 below its February peak, while architectural services employment added 900 new jobs in October (the most recent data available), bringing it to within about 10,000 positions of its pre-pandemic peak of 200,000, after losing nearly 17,000 jobs earlier this year.

In addition, according to the latest edition of the Federal Reserve’s Beige Book Report (released on December 2), most regions of the country experienced a modest to moderate expansion from late October into November, although some areas started to see growth slowing by mid-November as COVID-19 cases rose again. The report found that earlier optimism has waned in recent weeks, largely due to the recent virus surge as well as the forthcoming expiration of unemployment benefits and the moratorium on evictions and foreclosures. However, growth has continued to increase in certain sectors, namely homebuilding, existing home sales, manufacturing, and distribution and logistics. Regionally, the New York, Richmond, Atlanta, Kansas City, Dallas, and San Francisco Districts reported particularly strong conditions in their residential real estate markets, while softening commercial real estate markets were reported in the New York, Dallas, and San Francisco Districts, and the Richmond District reported that commercial real estate leasing was increasing in that region.

Varied firm outlooks for 2021

This month, we asked responding architecture firms to share their expectations for 2021, and what their biggest business-related concerns for the coming year are. Overall, firms are modestly optimistic – while just 7% expect that 2021 will be a great year for their firm, 39% expect that it will be a good year, and 25% predict a so-so year. However, 25% anticipate a challenging year, while 4% are worried that 2021 will be a potentially disastrous year for their firm. Notably, firms located in the Northeast, where conditions were weak even prior to the pandemic, expressed the most concern for 2021, while firms with a multifamily residential specialization were most likely to predict a good to great year ahead.

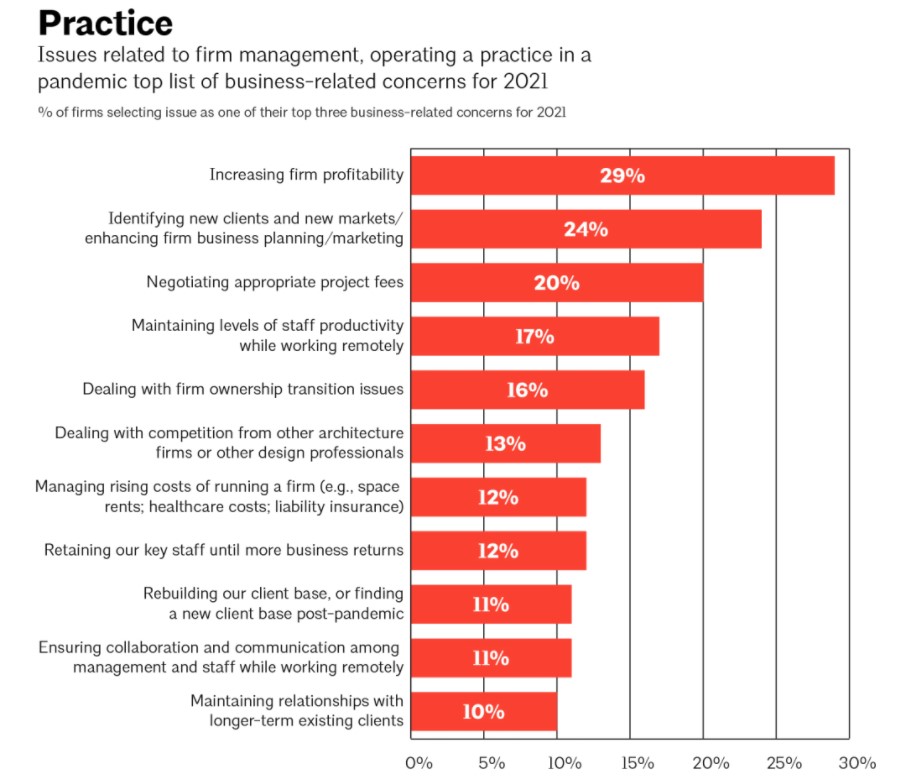

As far as the biggest business-related concerns for firms in 2021, increasing firm profitability remained the top concern again this year, cited as one of their top three concerns by 29% of responding firms. The top concerns cited by firms were split fairly evenly between general concerns about running their business and concerns related to the impact of the COVID-19 pandemic. Some of the other top concerns from last year, primarily related to issues around hiring and retaining staff, dropped off the list this year, amid the economic downturn and staff layoffs and furloughs.

Other top concerns related to project and firm management were about identifying new clients and new markets, enhancing firm business planning, and marketing (cited by 24% of firms as one of their top three concerns for 2021); negotiating appropriate projects fees (20% of firms); dealing with firm ownership transition issues (16% of firms); dealing with competition from other architecture firms/design professionals (13% of firms); and managing the rising costs of running a firm (12% of firms). Identifying new clients/new markets was of particular concern to firms with commercial/industrial and institutional specializations, since those have been hardest hit by the impact of the pandemic.

The top concerns cited that were related directly to the impact of the pandemic were issues generally related to staff management while working remotely, including maintaining levels of staff productivity while working remotely (17% of firms), retaining their key staff until more business returns (12% of firms), and ensuring collaboration and communication among management and staff while working remotely (11% of firms). Just over one in ten firms (11%) listed rebuilding their client base, or finding a new client base post-pandemic, as one of their top concerns, as firms indicated that they’ve had to shift to focus on new project types, or adjust their mix of projects, to weather the current downturn.

This month, Work-on-the-Boards participants are saying:

- “Our single-family residential work is extremely busy, while our commercial work is nonexistent. Almost all of our staff has been able to transition to the single-family side.”—10-person firm in the Midwest, mixed specialization

- “Business conditions are challenging but working in our favor is that Minority Business Enterprise (MBE) firms like us are being considered more equally than before.”—8-person firm in the Northeast, institutional specialization

- “Business is still strong here in Tennessee, and I expect 2021 to provide respectable growth for our firm. We are currently looking to hire two new people to accommodate the growth we see coming.”—23-person firm in the South, commercial/industrial specialization

- “2021 looks to be a very challenging year in the Puget Sound region. Public work has been curtailed significantly due to revenue shortfalls, and private development, outside of housing, seems to be waiting for a clear end to the pandemic.”— 55-person firm in the West, institutional specialization