ABI August 2022: Billings continue to grow at architecture firms

The following was originally published by AIA National.

Client willingness to invest in improving energy efficiency has increased in recent years

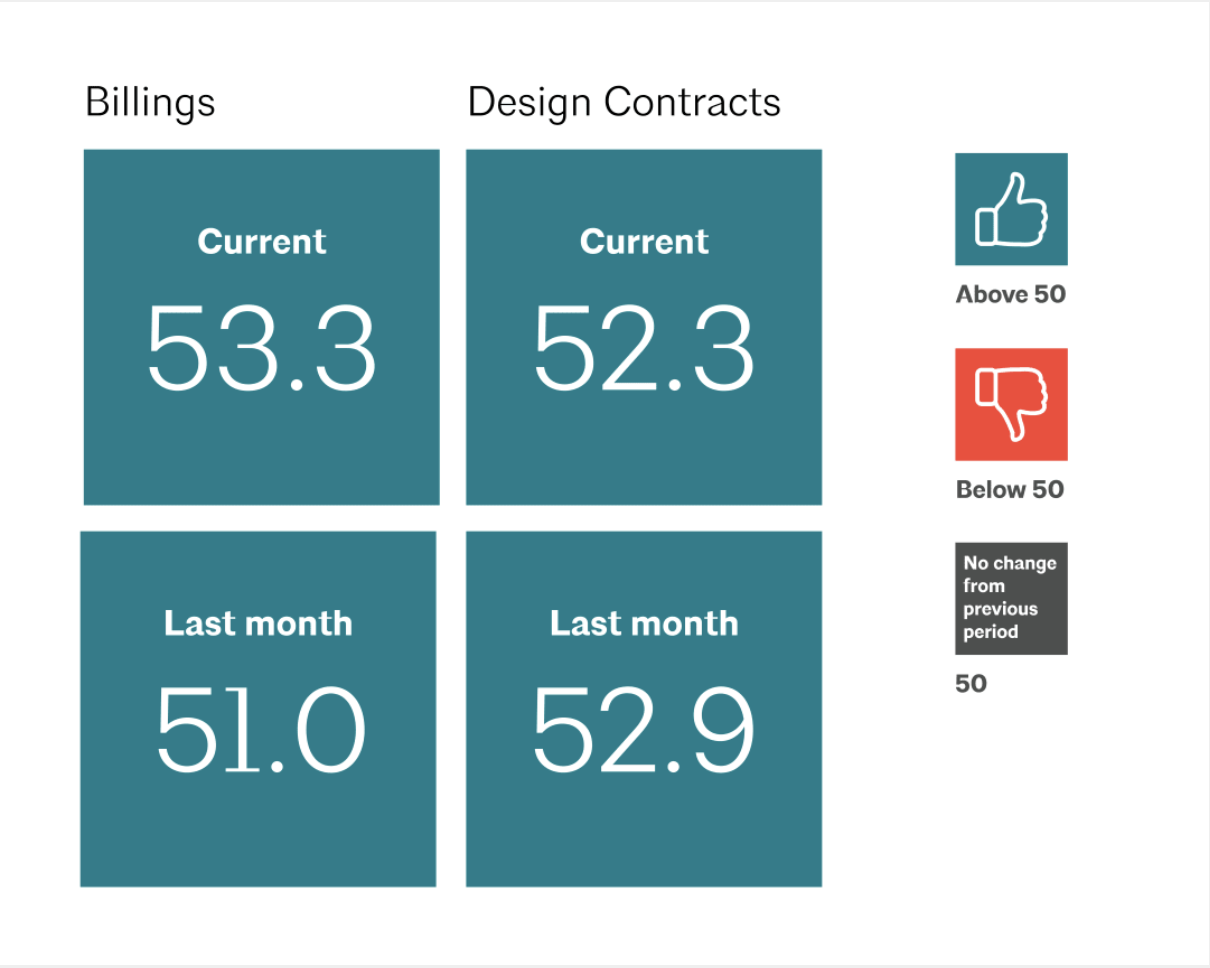

Business conditions remained generally strong at architecture firms in August. The Architecture Billings Index (ABI) score for the month ticked back up to 53.3 from 51.0 in July, as more firms reported an increase in billings. Inquiries into new projects also increased modestly in August from July, while the value of new design contracts held steady at the same rate of growth it has been at for the last two months. Many firms are still struggling to find enough employees to meet the amount of work they have coming in.

However, business conditions remain mixed by region of the country. Billings softened for the third consecutive month at firms located in the Northeast in August, and have declined for all but two months of the year so far. And while billings continued to rise at firms located in the West, fewer firms reported billings growth in August than they have in several months, and the pace of growth also declined slightly at firms located in the Midwest. Business conditions held steady at firms located in the South, where they were strongest overall for the second month in a row. In addition, firms of all specializations reported an increase in billings in August, with the strongest conditions reported by firms with multifamily residential and institutional specializations.

Federal Reserve expected to raise interest rates again in September

Conditions continued to be more mixed in the broader economy in August. Hiring remained strong, as nonfarm payroll employment grew by 315,000 positions, and architecture services employment added an additional 1,100 new positions in July, the most recent data available. However, inflation also continued to rise in August, when many had expected to see it level out or even start to decline. And while energy prices continued to moderate, they still remain far above the levels of one year ago, and food prices also continued to grow at a higher pace than expected. Because of this, the Federal Reserve is expected raise interest rates by yet another 0.75% during their meetings in late September, with some projections anticipating an increase of as high as 1.0%.

The latest edition of the Federal Reserve’s Beige Book report, released on September 7, also showed broadly mixed conditions across the country in the previous six weeks, with half of the districts reporting growth and the other half reporting softening conditions. Home sales fell in all 12 of the districts, and residential construction remained constrained by supply chain issues, which will only be exacerbated if a freight rail strike occurs. The report also showed broad softening in commercial real estate, particularly in demand for office space.

Firms report growing interest from clients in environmental performance investments

For this month’s special practice questions, we asked architecture firms about client willingness to invest in improvements related to environmental performance for their facilities. More than half of responding firms (55%) indicated that their clients have been more willing to invest in improving energy efficiency in recent years, with 16% saying that clients have been much more willing to invest. More than one third of firms also reported that their clients have been more somewhat or much more willing to make investments in incorporating lifecycle costing considerations in the design of project (37%) as well as increasing the use of safe and sustainable materials with reduced waste (36%). In contrast, nearly half of respondents (48%) indicated that their clients have been somewhat or much less willing to invest in achieving certification for a rating system (e.g., LEED; WELL) in the recent years.

Responding firms also reported that government clients at all levels (federal, state, and/or local) have been the most willing client type to make investments in their facilities to improve environmental performance, with 32% selecting them as the one most willing client type. Following government clients were educational institutions (28%), corporate owners of commercial properties (14%), and homeowners (11%) as the client types most willing to make investments to improve environmental performance. In addition, 9% of respondents selected healthcare institutions, 4% selected developers of commercial properties, and 2% selected industrial property owners as the client types generally most willing to make investments to improve environmental performance in their facilities.

Save the date! Join Kermit Baker, AIA’s Chief Economist, on Thursday, October 27 at 2 PM ET to hear the next quarterly update of the industry’s latest economic data and what firms are reporting. Register for free at https://aiau.aia.org/courses/2022-economic-update-4

This month, Work-on-the-Boards participants are saying:

- “Still very strong for us, even as the stories of a slowdown seem to build. Cashflow seems to be the issue at the moment, as budgets are busting and financing is more challenging”— 62-person firm in the Northeast, residential specialization

- “Planning department and environmental review times are being stretched out by governing agencies and delaying projects.”—12-person firm in the West, commercial/industrial specialization

- “Outstanding work opportunities since the automotive industry flipped the switch on electric vehicles.”—102-person firm in the Midwest, mixed specialization

- “Cost increases are causing a slowdown in client bond program pace, leading to slower decision-making and scope cuts to align with previously planned budgets that are now inadequate.”—80-person firm in the South, institutional specialization