ABI December 2020: Architecture firm billings end the year on a sour note

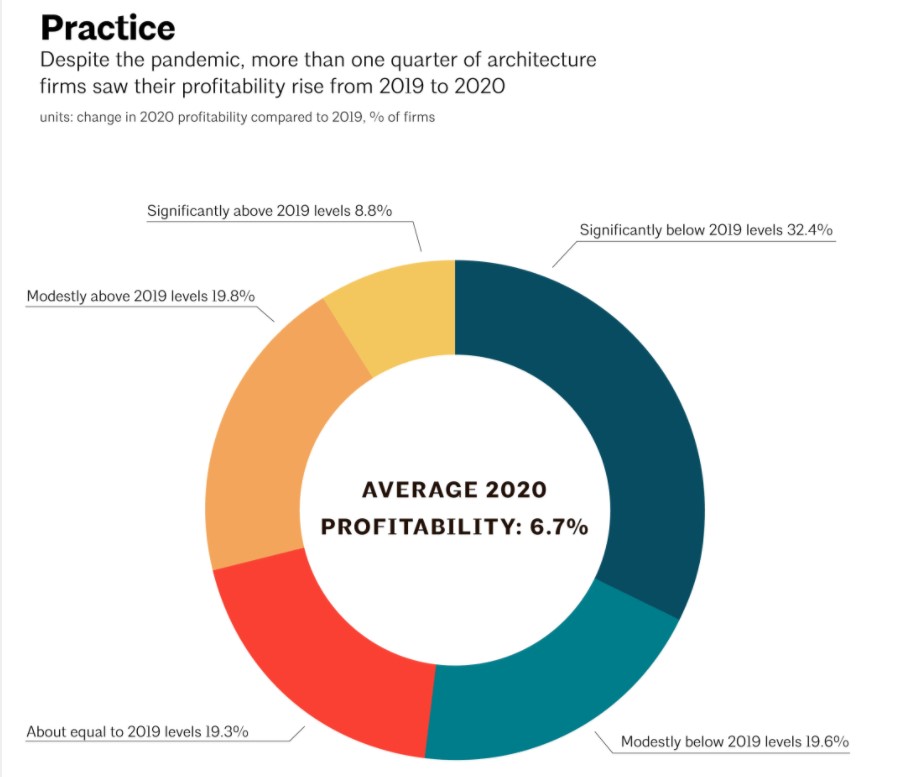

2020 firm profitability averaged 6.7%

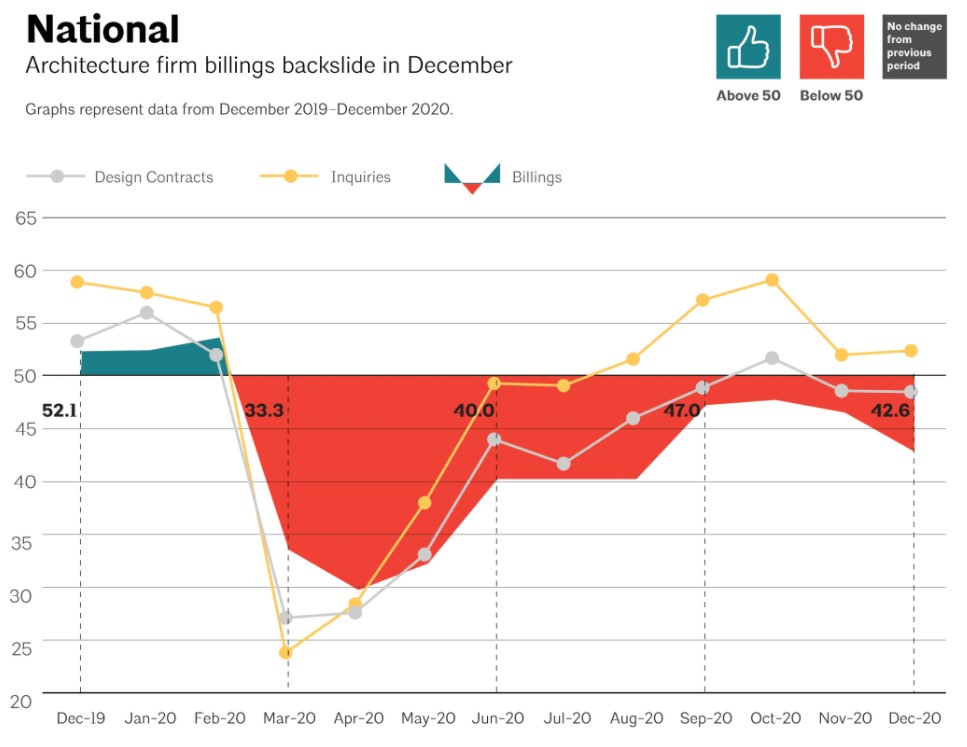

Business conditions at architecture firms backslid in December, ending a tough year on a disappointing note. The AIA’s Architecture Billings Index (ABI) score declined to 42.6 for the month, indicating that more firms saw declining billings in December than in November. Although some year-end softness is to be expected at many firms, the ABI analysis takes these seasonal factors into account, so it is unlikely the decline is due to just the typical December slowdown. Instead, ongoing uncertainty with an increase in COVID-19 cases and delays on the new stimulus package until late in the month are more likely contributors to the decline.

However, firms do remain relatively optimistic about 2021, and the indicators of future work tend to support that. Inquiries into new projects at firms increased for the fifth month in a row in December, and while the pace of growth was slower than in September and October, it still means that most firms are having project discussions with potential clients. And while the value of new design contracts decreased for the second consecutive month after rising in October, it remained near the 50 threshold, indicating that a nearly equivalent share of firms saw an increase in new contracts signed as saw a decrease. In addition, firm backlogs remained generally steady from the third quarter to the fourth quarter of 2020, declining slightly from an average of 5.4 to 5.3 months. This remains about a month below pre-pandemic backlog levels for the last two years, but has improved from the first quarter, where they fell all the way to 5.0 months from 6.3 months in the fourth quarter of 2019.

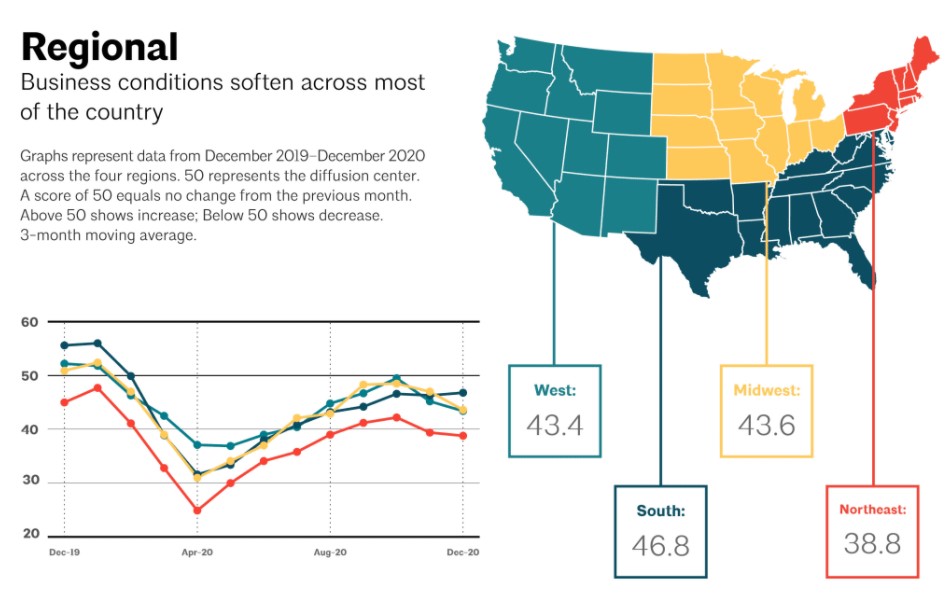

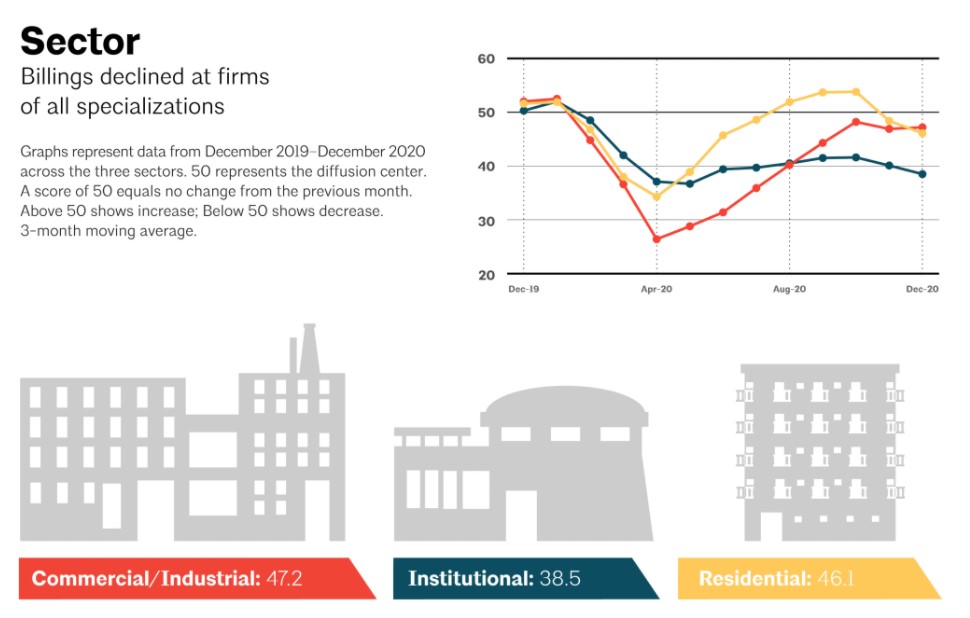

By region of the country, business conditions remained softest at firms located in the Northeast in December. The decline in firm billings was slightly less serious at firms located in the South, while conditions softened further at firms located in the Midwest and West. In addition, firms of all specializations saw billings decline this month, with billings slipping at firms with a multifamily residential specialization, which had seen a nice rebound in the late summer/early fall. Firms with a commercial/industrial specialization continued to approach a turnaround in business conditions, still largely led by increased demand for warehouse and distribution facilities.

Construction employment continues to rebound despite weakened economy

In the broader economy, conditions remained generally weak in December and into early January. Nonfarm payroll employment declined by 140,000 positions in December, the first month of losses since the early days of the pandemic in April. Construction employment has continued to rebound, however,, and added an additional 51,000 positions. Architectural services employment saw a modest decline of 400 positions in November, the most recent data available, and at 189,500 positions currently, remains above the most recent low point of 183,200 in July. And while the national unemployment rate held steady at 6.7% in December, the Department of Labor reported that initial unemployment claims rose to 965,000 the first week of January, reaching the highest level since last August.

2020 prosperity depended on firm size, specialization

This month’s special practice questions asked responding firms about their firm’s profitability in 2020, and the factors that impacted it. Overall, firms reported that their profitability softened from 2019 to 2020, with just over half of firms (52%) indicating that their profits were below 2019 levels, and nearly one third of firms (32%) reporting that their 2020 profitability was significantly below their 2019 level. However, more than a quarter of firms (28%) reported that their profitability in 2020 was above 2019 levels, and 20% reported that it was about equal to 2019 levels.

And on average, responding architecture firms reported a 2020 profitability rate of 6.7% (estimated as a percentage of their firm’s 2020 net billings after all compensation was paid, including owners’/principals’ compensation, but before paying out any taxes, discretionary bonuses, or profit-sharing). However, large firms (with annual billings of more than $5 million) and firms with a multifamily residential specialization had far more prosperous years, each reporting profitability rates approaching 12% (11.6% and 11.8%, respectively). Small firms and firms with a commercial/industrial specialization, on the other hand, reported profitability rates well below 5% (2.8% and 3.8%, respectively).

As far as the factors that were most important to their firm’s 2020 profitability, they were about evenly split between issues related to staff management and productivity and firm business challenges, as level of staff productivity and the number of projects that were delayed, stalled, or cancelled topped the list, with 37% and 36% of responding firms, respectively, selecting them as one of the three most important factors. In addition:

- 30% selected level of fees negotiated,

- 27% selected marketing and business development activities (and their impact on the number and/or quality of new projects that they were able to attract),

- 24% selected quality of staff,

- 24% selected ability to collect accounts receivable in a timely manner,

- 22% selected ability to communicate and collaborate with staff working remotely,

- 20% selected ability to manage existing projects,

- and 20% selected firm overhead costs as one of their top three most important factors affecting profitability in 2020.

This month, Work-on-the-Boards participants are saying:

- “Slowing down, but not significantly. Still a lot of pent-up energy and desire to ‘get back to business.’”—25-person firm in the Midwest, institutional specialization

- “Demand for residential properties is remarkably high even as institutional, hospitality, and retail operations are tremendously challenged economically.”—4-person firm in the Northeast, residential specialization

- “We are optimistic about work for 2021 but don’t expect profits to be as high as we would like – expect 5% or so.”— 36-person firm in the West, commercial/industrial specialization

- “Conditions appear to be better than they were six months ago, and we continue to be optimistic about 2021.”—50-person firm in the South, institutional specialization